WASHINGTON DC, Feb 13 (IPS) – Within the early Seventies, battle within the Center East set off a spike in oil costs that left central banks all over the world scrambling to regulate inflation. After a 12 months or so, oil costs stabilized and inflation began to retreat. Many nations believed that they had restored worth stability and loosened coverage to revive their recession-hit economies solely to see inflation return. Might historical past repeat?

World inflation reached historic highs in 2022 after Russia’s invasion of Ukraine triggered a terms-of-trade shock akin to that of the Seventies. Disruptions to Russian oil and gasoline provides added to COVID supply-chain issues to drive costs increased. In superior economies, costs rose on the quickest tempo since 1984. In rising market and creating economies, the value enhance was the most important for the reason that Nineties.

Aided by the sharpest rise in rates of interest in a era, inflation has began to subside finally. Headline inflation in the US and throughout a lot of Europe has halved from about 10 % final 12 months to lower than 5 % at this time. The newest battle within the Center East has, for now no less than, not had a big affect on oil costs. However it’s nonetheless too quickly for policymakers to have a good time victory over inflation.

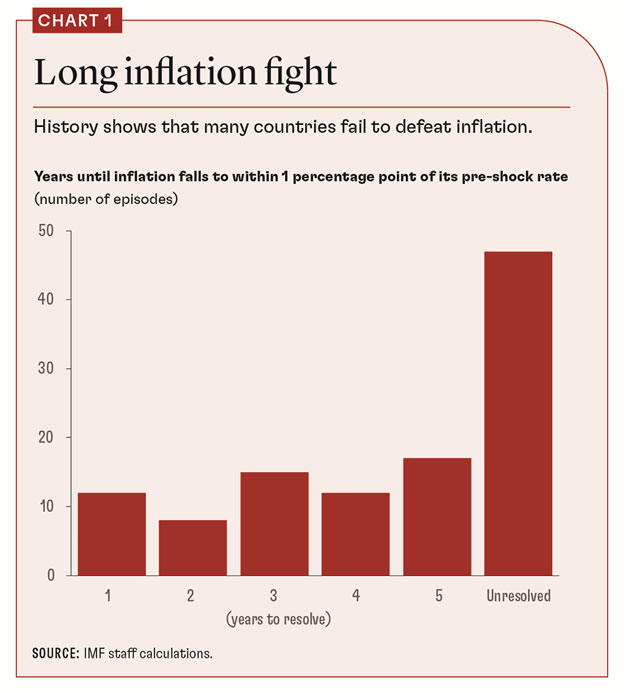

Our recent study of over 100 inflation shocks for the reason that Seventies presents two causes for warning. First, historical past teaches us that inflation is persistent. It takes years to “resolve” inflation by lowering it to the speed that prevailed earlier than the preliminary shock. Forty % of nations in our research didn’t resolve inflation shocks even after 5 years. It took the remaining 60 % a mean of three years to return inflation to pre-shock charges (Chart 1).

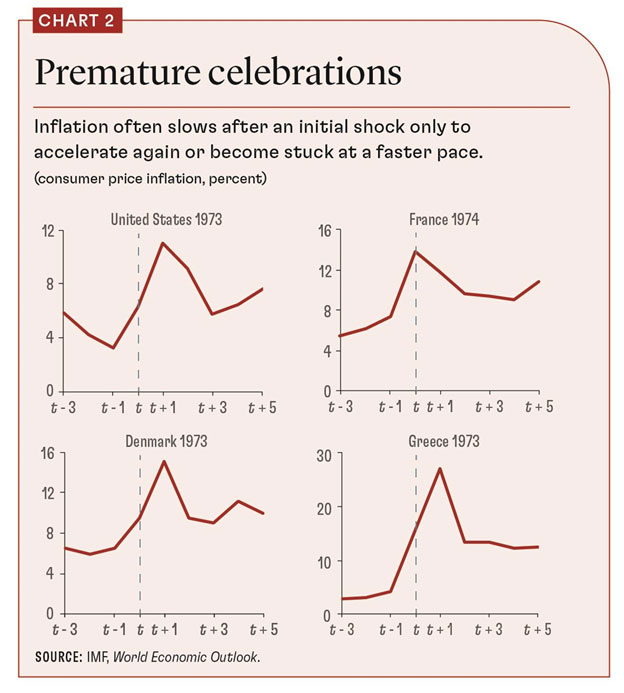

Second, nations have traditionally celebrated victory over inflation and loosened coverage prematurely in response to an preliminary decline in worth pressures. This was a mistake as a result of inflation quickly returned. Denmark, France, Greece, and the US had been amongst almost 30 nations in our pattern to loosen coverage prematurely after the 1973 oil-price shock (Chart 2).

In actual fact, nearly all nations in our evaluation (90 %) that didn’t resolve inflation noticed worth development gradual sharply within the first few years after an preliminary shock, solely to speed up once more or grow to be caught at a quicker tempo.

At the moment’s policymakers should not repeat their predecessors’ errors. Central bankers are proper to warn that the inflation combat is way from over, at the same time as latest readings present a welcome moderation in worth pressures.

Consistency and credibility

How ought to policymakers reply to persistent inflation? Once more, historical past gives some classes. The nations in our research that efficiently resolved inflation tightened macroeconomic insurance policies extra in response to the inflation shock and, crucially, maintained a good coverage stance persistently over a interval of a number of years.

Examples right here embrace Italy and Japan, which adopted tighter-for-longer insurance policies after the 1979 oil-price shock. Against this, nations that didn’t resolve inflation had looser coverage stances and had been extra prone to change between tightening and loosening cycle (Chart 3).

Coverage credibility issues, too. Nations the place inflation expectations had been extra firmly anchored, or the place central banks had extra success sustaining low and secure inflation previously, had been extra prone to defeat inflation.

At the moment’s policymakers can take some solace from this discovering. Central bankers in lots of nations could discover it simpler to defeat inflation this time due to the coverage credibility they’ve constructed up over a number of many years of profitable macroeconomic administration. With the best insurance policies in place, nations may resolve inflationary pressures ahead of previously.

However it gained’t be simple. Situations within the labor market particularly require shut consideration. In lots of nations, employees’ wages have fallen in actual inflation-adjusted phrases and will have to rise once more to meet up with increased costs. But wage development may gasoline inflation whether it is too excessive and will result in pernicious wage-price spirals.

Traditionally, nations that resolved inflation efficiently tended to have decrease nominal wage development. Importantly, this didn’t translate into decrease actual wages and a lack of buying energy, as a result of decrease nominal wage development was accompanied by cheaper price development.

The implication for policymakers right here is to stay targeted on actual wages, not nominal wages, when responding to developments within the labor market.

Nations that resolved inflation efficiently had been additionally higher at sustaining exterior stability. Free-floating currencies had been much less prone to depreciate sharply, and forex pegs had been extra prone to survive. This isn’t a name for forex intervention.

As a substitute, it seems that nations’ success in preventing inflation—by means of tighter financial coverage and higher coverage credibility—was instrumental in shoring up alternate charges. Nations that enable inflation to linger in the end pay a better worth.

The final word prize

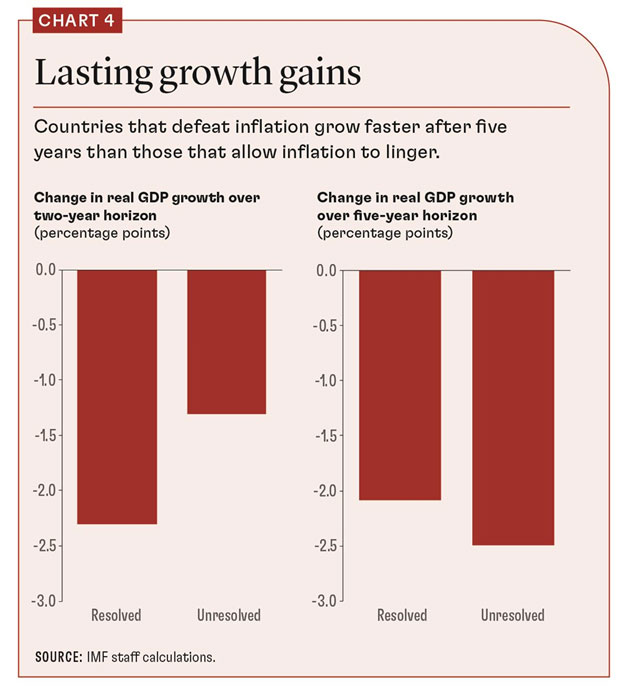

Preventing inflation is tough. However you will need to acknowledge the advantages of worth stability. Traditionally, nations that resolved inflation had decrease financial development within the brief time period than those who didn’t. However this relationship reversed over the medium and long run.

5 years after the inflation shock, nations that resolved inflation had increased development and decrease unemployment than economies that allowed inflation to linger.

The economics behind this discovering are intuitive. There’s a trade-off between bringing inflation down on one hand and reaching increased development and decrease unemployment on the opposite. However this trade-off is non permanent: development recovers and jobs are created as soon as inflation is introduced beneath management.

Against this, leaving inflation unresolved comes with its personal prices of macroeconomic instability and inefficiency. These prices accumulate for so long as inflation stays excessive. Consequently, cumulative welfare losses from unresolved or completely excessive inflation dominate over the medium to long run (Chart 4). Nations that enable inflation to linger in the end pay a better worth.

Central bankers are on the entrance line of the combat in opposition to inflation and will pay probably the most consideration to those classes. However governments should not make the duty of financial authorities more durable by including to cost pressures with free fiscal coverage.

To make fiscal assist throughout a cost-of-living disaster much less inflationary, governments ought to goal aid to probably the most susceptible, the place it’s going to alleviate struggling most.

The previous is rarely an ideal information to the current, as a result of no two crises are exactly alike. All the identical, historical past presents clear classes to policymakers at this time. Preventing inflation is a marathon, not a dash. Policymakers should persevere, show coverage credibility and consistency, and hold their eyes on the prize: macroeconomic stability and stronger development caused by returning inflation firmly to focus on.

If historical past is a information, inflation’s latest decline may very well be transitory. Policymakers could be smart to not have a good time too quickly.

Supply: IMF Finance and Improvement

Anil Ari is an economist within the IMF’s Technique, Coverage, and Assessment Division; Lev Ratnovski is an economist within the IMF’s European Division.

The opinions expressed are these of the authors; they don’t essentially mirror IMF coverage. This text attracts on IMF Working Paper 2023/190, “One Hundred Inflation Shocks: Seven Stylized Information,” by Anil Ari, Carlos Mulas-Granados, Victor Mylonas, Lev Ratnovski, and Wei Zhao.

IPS UN Bureau

© Inter Press Service (2024) — All Rights ReservedOriginal source: Inter Press Service

{kind=link}